Don't Let a Hail Storm Dent Your Savings

Currently available in: Arkansas, Colorado, Georgia, Indiana, Iowa, Kansas, Kentucky, Missouri, Ohio, Oklahoma, Tennessee and Texas

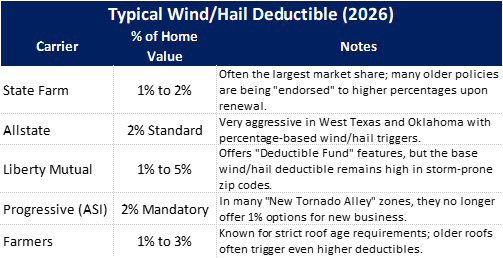

Traditional Home Insurance...

While your main policy covers major disasters, it often leaves you with a wind or hail deductible that is massively larger than the deductible for all other risks.

Also, homeowners insurance won’t pay for things like tree and debris removal, replacing spoiled food, power restoration or temporary living expenses (prior to making a claim).

Madrona Wind and Hail Insurance...

The first few days after a storm can be paralyzing. Don’t let a high wind/hail deductible stall your home’s recovery. At less than $180 a year, or $0.50 a day for a $5,000 payout, our policy provides the immediate liquidity you need to start repairs after a storm.

We bridge the gap between disaster and restoration. It’s the smartest way to ensure a storm never hits your bank account as hard as it hits your roof.

After a Storm, Traditional Home Insurance...

Requires you to pay the deductible first (often thousands of dollars), then file a claim, wait for an adjuster, negotiate depreciation, and eventually receive a check.

After a Storm, Madrona Wind and Hail Insurance...

Relies on National Weather Service data to identify and pay wind/hail claims. We have partnered with the first carrier to use this data to avoid adjustors, reduce costs for our customers and provide an easier claims experience.

Traditional Home Insurance - Making a Claim

Before calling the insurance company, most homeowners call a local roofer to confirm if the damage exceeds the deductible. If the damage is worth $1,500 but the deductible is $2,500, it’s usually not worth filing a claim.

Then a claim number and an adjuster is assigned… and the waiting game begins. During a major storm event, it can take 1–3 weeks just to get an adjuster to the property.

Once they arrive:

If you have an older roof, the insurance company may only pay for its depreciated value. You might receive a check for $4,000 for a roof that costs $12,000 to replace today.

Cosmetic Exclusions: Many modern policies now include “cosmetic damage exclusions,” meaning if the hail dents your metal roof or siding but doesn’t “break the seal” or cause a leak, the insurance company may deny the claim entirely, leaving you with the aesthetic damage.

Madrona Wind and Hail Insurance - Making a Claim

Start your claim in minutes, go to your Policyholder Portal and click “File Claim” to tell us about the event type, event date, any description, and any photos of damage. NO receipts or quotes to submit.

We use data to confirm storm activity in your area. Weather data takes some time to be released. We will keep you updated along the way.

Get Paid Fast – When your claim is approved, funds are deposited directly into your bank account – In less time than it takes to get the adjustor to your home, typically 7 to 10 days once weather data is confirmed.

Plus, the payout is yours to use however you choose, whether that is covering your homeowners deductible, paying for repairs, or handling other storm-related expenses.

Traditional Home Insurance - Costs

- Uses Percentage of Home Value for wind and hail deductible

- Every claim you file is recorded and remains for 5 to 7 years.

- Insurers often raise premiums after a claim is filed.

- Two weather claims within a three-year period, may label you “high risk.” This can lead to a non-renewal notice.

Madrona Wind and Hail Insurance - Costs

- There is no deductible

- A “claim” is not recorded

- A payout will not impact your home insurance premiums.

- We do not non-renew a policy or increase the premium after a claim. Policy cost is only based on your home’s risk, not your personal details nor whether or not you filed a claim.

Good to Know:

- Hail/Wind insurance is a companion policy to your homeowners insurance not a replacement.

- The policy must be in an individual’s name (not an LLC or corporation).

- It does not cover hurricanes nor named storms.

- Policies have a 5-day waiting period before coverage begins.

- Eligible for up to two payouts per policy term. After a payout, there is a 30-day waiting period before coverage resets.

- Hail Payouts: A payout is triggered if hail is 1.75 inches or larger, or if the “Hail Score” shows a 65% or higher probability of damage.

- Wind Payouts: Payouts are based on a sliding scale according to wind speed (EF levels).