Parametric, What?

What Is A Parametric Policy, And How Does It Work?

What It Is:

Parametric insurance is a specialized type of coverage that pays out a fixed, predetermined amount based on the intensity or metrics of an event. Unlike traditional insurance, which requires a lengthy adjustment process to calculate your exact financial loss, parametric coverage is entirely data-driven. Also, parametric policies are Standalone policies, not a buyback and thus NOT tied to your homeowner's policy

How It Works: The Three Components

The Trigger: Coverage is tied to objective, third-party data—such as a specific wind speed (e.g., 74+ mph), hail size (e.g., 2 inches), or a storm's category ranking.

The Location (The Index): The policy uses precise geographical data, often tracking whether the storm's path or wind field entered your home's exact GPS coordinates or a small geographic grid around it.

The Payout: Proof (pictures of damage) is submitted and if the data shows the weather event met or exceeded the trigger criteria at your location, the policy pays, either a percentage or all. The payout amount is fixed in advance, so there is no negotiation or assessment, period.

Key Benefits

Speed: Because there is no need for a physical damage inspections by a contractor or adjuster, money often lands in your account within a few days of the storm.

Total Spending Flexibility: Standard homeowners insurance restricts payouts to fixing covered structural property damage. Parametric payouts are pure cash. You can use it to cover a massive wind/hail percentage deductible, pay for immediate tree debris removal, buy a generator, or fund an evacuation.

How Payouts Work:

The Peril: Wind / Tornado / Hail

The Peril: Hurricane

1. Hail Events

Instead of assessing the exact physical damage, this policy utilizes a proprietary “Hail Score” based on National Weather Service (NWS) data that measures hailstone size, density, and storm duration. If a hailstorm drops stones 1.75 inches or larger, or if the storm hits a 65% or higher hail score, you receive the full payout up to your policy limit.

For wind damage, payouts are tiered automatically based on the Enhanced Fujita (EF) scale measured at your property’s exact location:

- EF0 to EF1 (86–110 mph): Partial payout (e.g., $3,000 on a $25k policy =12%)

- EF2 (111–135 mph): Partial payout (e.g., $5,000 on a $25k policy = 20%)

- EF3 (136–165 mph): Partial payout (e.g., $10,000 on a $25k policy = 40%)

- EF4 (165–200 mph): Partial payout (e.g., $15,000 on a $25k policy = 60%)

- EF5 (200+ mph): Full policy limit paid = 100%

Three Triggers to Choose From:

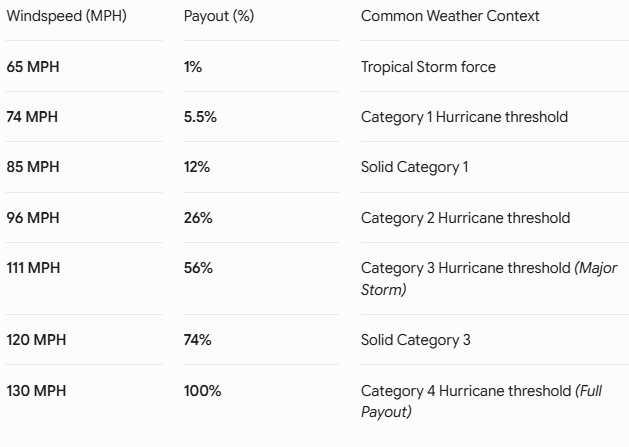

Using three independent triggers—rather than a single measure—helps the likelihood of a payout triggering in the event of a hurricane. You will receive the highest payout for the selected triggers (starting at Windspeeds of 65mph):

Single: Proxy via Moody’s H-Wind (used by National Weather Service) – A 60 second wind speed reading from reliable third-party data sources; Good

Dual: Proxy+Anemometer Network (managed by WeatherScope) – Anemometers provide on-the-ground wind speed measurements, further refining accuracy (second opinion); Better

Triple: Proxy+Anemometer+Cat-in-a-Circle (15-mile radius) – Trigger based on the eye of the hurricane entering the circle. Best

Payouts scale up automatically with storm severity. It starts with a 1% cash injection at 65 MPH to handle minor immediate needs, scales up to a 56% payout the moment a Category 3 hurricane hits, and maximizes to a full 100% cash payout at 130 MPH.

Claim Rules for Wind / Tornado / Hail:

Limits: You are eligible for up to two payouts per policy term. After receiving a payout, there is a mandatory 30-day waiting period for your coverage to reset.

Usage: You are not restricted on how you spend the money; you can use it to cover your primary insurance deductible, handle emergency temporary repairs, or pay for a total roof replacement.